Schedule a Consultation: 858.483.9200

Why is a Professional Practice Not Permitted to Use a Foreign LLC or PLLC in California?

Choosing the right business structure is a critical decision for licensed professionals establishing their private practices in California. While foreign limited liability companies (foreign LLCs) foreign professional limited liability companies (foreign PLLCs) and are popular outside of California for their flexibility and tax benefits, professional practices in California are expressly prohibited from operating as a foreign limited liability company (foreign LLC) or foreign professional limited liability company (foreign PLLC).

While the question, “why is a professional practice not permitted to use a foreign LLC or PLLC?” has been answered in previous articles cited and summarized below, the experienced corporate attorneys at San Diego Corporate Law receive inquiries on a weekly basis from professional receiving mixed information from other attorneys or advisors leading them to believe that in certain circumstances it might be permissible to practice in a foreign LLC or foreign PLLC in California.

This article references and links to previous articles with regard to the business structures and business entities professionals may use to practice in California, but the purpose of this article is to highlight and explore the specific provisions of the California Corporations Code that prohibits the use of foreign LLCs and foreign PLLCs to render professional services as a professional in California.

California Corporations Code Section 13401

The Moscone-Knox Professional Corporations Act is found in California Corporations Code Sections 13400-13410. California Corporations Code Section 13401(b) provides the authority for licensed professionals to practice in California as California Professional Corporations with the purpose of rendering professional services in their California practice.

California Corporations Code Section 13401 also provides two definitions required to properly analyze the restrictions on the use of foreign LLCs and foreign PLLCs by licensed professionals practicing in California.

California Corporations Code Section 13401(a)

California Corporations Code Section 13401(a) provides the definition of “Professional Services” as follows:

“‘Professional services’ means any type of professional services that may be lawfully rendered only pursuant to a license, certification, or registration authorized by the Business and Professions Code, the Chiropractic Act, or the Osteopathic Act.”

Thus, Professional Services under the definition provided by California Corporations Code Section 13401(a) encompasses many professions, including without limitation as follows:

Accounting (California Business and Professions Code Sections 5150–5158);

Acupuncture (California Business and Professions Code Sections 4975–4979);

Architecture (California Business and Professions Code Sections 5610–5610.7);

Audiology (California Business and Professions Code Sections 2536–2537.4);

Chiropractic (California Business and Professions Code Sections 1050–1058);

Licensed Professional Clinical Counselor (California Business & Professions Code Sections 4999.123-4999.129);

Clinical Social Work (California Business and Professions Code Sections 4998–4998.5);

Dental Hygienist in Alternative Practice (California Business and Professions Code Sections 1967–1967.4);

Dentistry (California Business and Professions Code Sections 1800–1808);

Law (California Business and Professions Code Sections 6127.5, 6160–6172);

Marriage and Family Therapy (California Business and Professions Code Sections 4987.5–4988.2);

Medicine (California Business and Professions Code Sections 2400–2417.5);

Midwifery (California Business and Professions Code Sections 2505–2523);

Naturopathic Doctors (California Business and Professions Code Sections 3670–3675);

Nursing (California Business and Professions Code Sections 2775–2781);

Occupational Therapy (California Business and Professions Code Sections 2570 – 2572);

Optometry (California Business and Professions Code Sections 3160–3167);

Osteopathy (California Business and Professions Code Sections 2400–2417.5, 3600);

Pharmacy (California Business and Professions Code Sections 4150-4156);

Physical Therapy (California Business and Professions Code Sections 2690–2696);

Physician Assistants (California Business and Professions Code Sections 3540–3545);

Podiatry (California Business and Professions Code Sections 2400–2417.5);

Psychology (California Business and Professions Code Sections 2907–2913, 2995–2999);

Shorthand Court Reporters (California Business and Professions Code Sections 8040–8051);

Speech-Language Pathology (California Business and Professions Code Sections 2536–2537.4); and

Veterinarians (California Business and Professions Code Sections 4910–4917).

California Corporations Code Section 13401(d)

California Corporations Code Section 13401(d) provides the definition of “Licensed Person” as follows:

“‘Licensed person’ means any natural person who is duly licensed under the provisions of the Business and Professions Code, the Chiropractic Act, or the Osteopathic Act to render the same professional services as are or will be rendered by the professional corporation or foreign professional corporation of which the person is, or intends to become, an officer, director, shareholder, or employee.”

Thus, Licensed Person under the definition provided by California Corporations Code Section 13401(d) means those persons licensed in the professions listed above as providers of Professional Services under California Corporations Code Section 13401(a).

California Corporations Code Section 17701.04

Two subsections of California Corporations Code Section 17701.04 explicitly outline restrictions on the use of a foreign LLC or foreign PLLC for the provision of professional services.

Professional Services, as defined under California Corporations Code Section 13401(a), refers to professional services that require a license, certification, or registration by governmental agencies or other entities and regulatory boards in California. California Corporations Code Section 17701.04 establishes that individuals or entities practicing as a professional in California cannot form a foreign LLC or foreign PLLC for these purposes.

California Corporations Code Section 17701.04(b)

One of the primary legal barriers to professional practices utilizing a foreign LLC or foreign PLLC can be found in California Corporations Code Section 17701.04(b), which reads:

“A limited liability company may have any lawful purpose, regardless of whether for profit, except the banking business, the business of issuing policies of insurance and assuming insurance risks, or the trust company business. A domestic or foreign limited liability company may render services that may be lawfully rendered only pursuant to a license, certificate, or registration authorized by the Business and Professions Code, the Chiropractic Act, the Osteopathic Act, or the Yacht and Ship Brokers Act, if the applicable provisions of the Business and Professions Code, the Chiropractic Act, the Osteopathic Act, or the Yacht and Ship Brokers Act authorize a limited liability company or foreign limited liability company to hold that license, certificate, or registration.”

California Corporations Code Section 17701.04(b) is one of the more confusing sections in the analysis of restrictions on using a foreign LLC or foreign PLLC for professional practice in California. While the first half of the second sentence of California Corporations Code Section 17701.04(b) does read:

“A domestic or foreign limited liability company may render services that may be lawfully rendered only pursuant to a license, certificate, or registration authorized by the Business and Professions Code, the Chiropractic Act, the Osteopathic Act, or the Yacht and Ship Brokers Act…”

the second half of that sentence requires there to be applicable provisions the California Business and Professions Code or other applicable Act to actually authorize the use of a foreign LLC or foreign PLLC, which authorizing provisions are rare at the time of this writing for the practice of a profession in California. One such example, limited to shorthand court reporters only, is found in California Business and Professions Code Section 8051, but examples such as this are few and far between.

California Corporations Code Section 17701.04(e)

Another of the legal barriers to a professional practice utilizing a foreign LLC or foreign PLLC for a profession practice in California can be found in California Corporations Code Section 17701.04(e), which reads:

“Nothing in this title shall be construed to permit a domestic or foreign limited liability company to render professional services, as defined in subdivision (a) of Section 13401 and in Section 13401.3, in this state.”

This section of the California Corporations Code explicitly prohibits foreign LLCs and foreign PLLCs from providing Professional Services in California under California Corporations Code 13401(a) by Licensed Persons under the definition of California Corporations Code Section 13401(d).

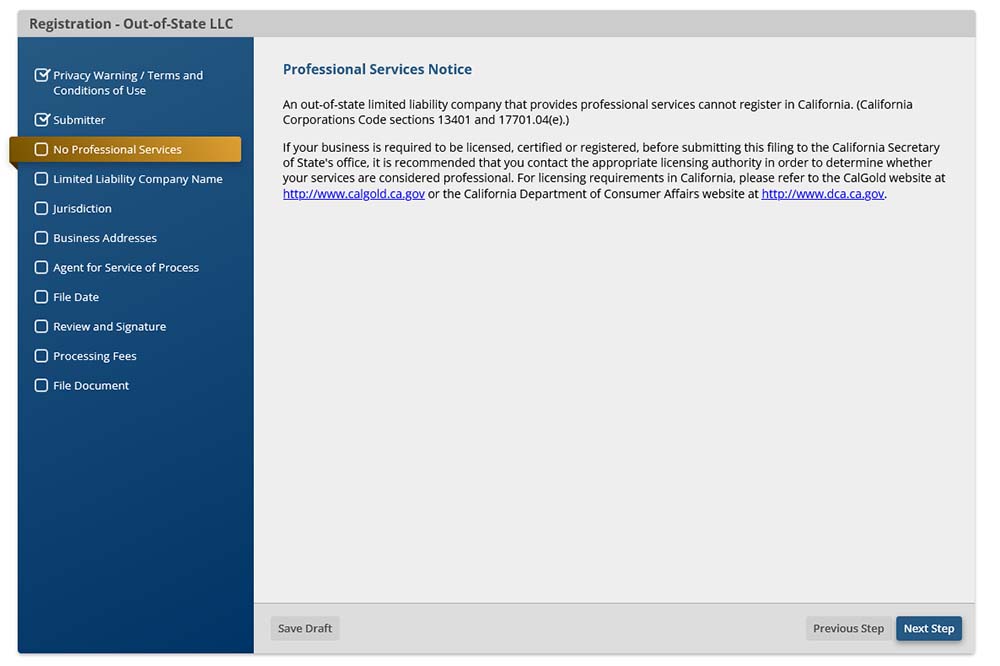

Secretary of State Application to Register a Foreign LLC for Authority to Transact Business in California for a Professional Practice

California Registration – Out-of-State LLC Screenshot of Professional Services Notice

As shown in the image above, in order to register a foreign LLC or foreign PLLC for authority to transact business in California with the California Secretary of State (commonly referred to as foreign registration), the filer must agree to the following provision:

“An out-of-state limited liability company that provides professional services cannot register in California (California Corporation Code section 13401 and 17701.04(e). If your business is required to be licensed, certified or registered, before submitting this filing to the California Secretary of State’s office, it is recommended that you contact the appropriate licensing authority in order to determine whether your services are considered professional. For licensing requirements in California, please refer to the CalGold website at http://www.calgold.ca.gov or the California Department of Consumer Affairs website at http://www.dca.ca.gov.”

A filer may successfully file the Application for Registration for Authority to Transact Business in California despite the warning depicted and quoted above, however, acceptance of the Application for Registration for Authority to Transact Business in California by the Secretary of State does not constitute the consent of the California Secretary of State to practicing with a foreign LLC or foreign PLLC under the California Corporations Code.

Reasons for Prohibition Against a Foreign Limited Liability Company or Foreign Professional Limited Liability Company for California Professionals

The main reason for prohibiting the use of foreign LLCs and foreign PLLCs by licensed professionals is to ensure compliance with professional regulations and protect the public from potential harm caused by unqualified or unethical individuals providing professional services by upholding public accountability standards specific to the practice in California. The State of California wants to ensure that only licensed professionals who have met certain education and training requirements are able to offer their expertise and advice in a professional capacity as a licensed professional.

The reasoning behind this restriction stems from the nature of professional services, which requires specialized knowledge and experience, and is subject to stringent regulation by the State of California and the governing boards of each profession. Professions demand accountability not just to patients or clients, but also to their professional licensing boards.

Foreign LLC and foreign PLLC structures, known for their liability protections and manager/member flexibility, are deemed incompatible with the heightened accountability standards the State of California applies to licensed professionals. Thus, professionals practicing in California must choose alternative structures that better align with the regulatory oversight and public protection goals of the State of California.

California Professional Corporations require adherence to stricter regulations regarding ownership and governance. Licensed professional shareholders of a California Professional Corporation must be licensed to practice the profession and certain other licensed professionals permitted under California Corporations Code Section 13401.5 may also be shareholders (see: “Who May Be a Shareholder of a California Professional Corporation?“), ensuring that ethical standards and professional expertise guide the practice in California.

For attorneys and accountants, a California LLP also provides liability protection for licensed professional partners while keeping the spotlight on professional responsibility.

Permitted California Business Structures for Licensed Professionals

Licensed professionals in California are restricted in the types of business entities they may form due to California law in the California Corporations Code discussed above. These California laws are designed to ensure compliance with professional standards of practice and maintain accountability for practicing in California.

A previous article titled “Can I Use a PLLC in California?” (which is as equally applicable to foreign LLCs as it is foreign PLLCs) answered the question of whether a licensed professional could use a foreign LLC or foreign PLLC in California, discusses some of the possible alternatives to practicing as a foreign LLC or foreign PLLC.

This section will provide an overview of the permitted business structures that licensed professionals may utilize, including California Professional Corporations, partnerships, and sole proprietorships, while providing links to articles containing more information about the specific requirements and considerations for each business entity structure.

Sole Proprietorships for California Licensed Professionals

A sole proprietorship is the simplest business structure for licensed professionals to practice in California, but it does come with some downsides. It is an unincorporated business owned and operated by the licensed professional personally, making it straightforward to set up and maintain, but it provides no liability protection or tax benefits. For licensed professionals in California, understanding how a sole proprietorship functions and the associated considerations is critical to ensuring compliance and achieving success.

Key Features of Sole Proprietorships for California Licensed Professionals

One of the primary advantages of a sole proprietorship is ease of formation. There are minimal regulatory requirements compared to other business structures, which reduces the time and cost of starting a practice. Sole proprietors simply need to obtain the appropriate professional licenses and any required local permits to begin operations.

Another notable feature of a sole proprietorship is that the licensed professional has complete control of the business. This autonomy allows licensed professionals to make decisions and manage their practice without needing approval from partners or shareholders.

However, sole proprietors are personally liable for all debts and obligations of their business. For California licensed professionals, this means that personal assets can be at risk if claims arise from professional services or other business activities. It is crucial for sole proprietors to consider obtaining adequate liability insurance to mitigate this risk.

Tax Considerations of Sole Proprietorship for Practicing Professionally

From a tax perspective, sole proprietorships are treated as “pass-through” entities. This means the business income is reported directly on the owner’s personal tax return, simplifying the tax filing process. However, sole proprietors are subject to self-employment taxes, which includes both the employer and employee portions of Social Security and Medicare taxes.

Is a Sole Proprietorship Right for You?

While a sole proprietorship may offer simplicity and independence, it is essential to weigh the potential risks and benefits relative to other business structures, such as California Professional Corporations. Licensed professionals should assess their long-term business goals, liability exposure, and the administrative requirements when selecting a business entity. For more detailed guidance on sole proprietorships for licensed professionals in California, consult “Sole Proprietorship vs Professional Corporation in California” and “What are the Business Structure Options for Solo Professionals in California?” or schedule a consultation with the experienced corporate attorneys at San Diego Corporate Law to ensure compliance and alignment with your professional objectives.

Partnerships for California Licensed Professionals

A partnership is one of the simplest business entity structures available for two or more licensed professionals looking to collaborate professionally. For California professionals, partnerships may offer a straightforward structure for operating a professional practice. However, it is essential to understand the benefits, limitations, and regulatory implications before forming a partnership for practicing in California.

Key Features of Partnerships for California Licensed Professionals

A California General Partnership is formed when two or more individuals agree to engage in a business together for profit, without formally organizing another form of business entity. Partners share ownership, responsibilities, profits, and liabilities equally unless otherwise agreed upon through a written partnership agreement. Importantly, in California, general partnerships do not require registration with the state to be established, but they must comply with local licensing and regulatory requirements applicable to the profession practiced in California. Partners of a California General Partnership have joint and several liability for all debts, liabilities, obligations, and legal judgments against the California General Partnership.

For accountants and attorneys, a California Limited Liability Partnership (California LLP) is an attractive alternative to a California General Partnership. Although similar in the sharing of ownership, responsibilities, and profits between partners like a California General Partnership, in a California LLP partners enjoy limited liability protection because they do not usually have personally liable for the malpractice of other partners, employees, or independent contractors of the California LLP, but California LLP partners still have joint and several liability for all other debts, liabilities, obligations, and legal judgments against the California LLP.

Tax Considerations of Partnerships for Practicing Professionally

One of the main considerations when choosing between these a partnership for a professional practice is the tax implications.

Partnerships are subject to pass-through taxation, a process that allows the income, deductions, and tax credits of the partnership to “pass through” to the individual partners rather than being taxed at the business entity level. This means that the partnership itself does not pay federal income taxes. Instead, each partner reports their share of the profits or losses of the partnership on their personal income tax return, based on their ownership interest.

In addition to income taxes, partners of a partnership are generally considered self-employed for tax purposes. This designation requires them to pay self-employment taxes, which cover Social Security and Medicare contributions. Unlike employees, who split these taxes with their employer, self-employed individuals are responsible for the full tax rate, currently 15.3% of net earnings. The self-employment tax liability of each partner is calculated based on their share of the net income of the partnership.

It is crucial for professionals considering a partnership business structure for their professional practice to understand the income tax and self-employment tax obligations of partnerships and plan accordingly, as these taxes can significantly impact personal income tax liability.

Is a Partnership Right for You?

While a partnership may offer simplicity and independence, it is essential to weigh the potential risks and benefits relative to other business structures, such as California Professional Corporations. Licensed professionals should assess their long-term business goals, liability exposure, and the administrative requirements when selecting a business entity for their professional practice. For more detailed guidance on California General Partnerships and California LLPs for licensed professionals in California, consult “What are the Business Structure Options for Group Practices in California?” or schedule a consultation with the experienced corporate attorneys at San Diego Corporate Law to ensure compliance and alignment with your professional objectives.

California Professional Corporations for California Licensed Professionals

In California, licensed professionals have the option to form a California Professional Corporation with the California Secretary of State as the business entity structure to practice in California. A California Professional Corporation is a specialized type of California Corporation that is specifically designed for licensed professionals.

Key Features of California Professional Corporations for California Licensed Professionals

One of the main advantages of forming a California Professional Corporation is that it offers personal liability protection for the licensed professional shareholders who own the California Professional Corporation. This means that all debts, liabilities, obligations, and legal judgments against the professional practice that are not subject to a personal guaranty or based on malpractice or professional errors and omissions will stay with the California Professional Corporation and not flow to the licensed professional shareholder (see: “What Liability Protection Does a California Professional Corporation Provide?“).

However, there are certain restrictions on who can own and manage a California Professional Corporation which require only licensed professionals and certain licensed persons permitted under California Corporations Code Section 13401.5 to be shareholders (see: “Who May Be a Shareholder of a California Professional Corporation?“).

Tax Considerations of California Professional Corporations for Practicing Professionally

Forming a California Professional Corporation can also provide tax benefits to licensed professional shareholders (see: “What Tax Benefits Does a California Professional Corporation Provide?“). For example, a California Professional Corporation can make an S Corporation election, which allows for pass-through taxation (see: “Can a California Professional Corporation Be an S-Corp?“). Electing to be taxed as an S-Corp means that the profits and losses of a California Professional Corporation are passed through to the personal tax returns of the individual shareholders rather than being subject to double taxation at both the corporate and individual level.

Additionally, California Professional Corporations do not subject licensed professional shareholders to self-employment taxes, and licensed professional shareholders who also provide professional services must only pay payroll taxes on that portion of their income from the California Professional Corporation that are paid as W-2 wages.

It is important for professionals to consult with a tax advisor when considering forming a California Professional Corporation, as both the personal financial situation of the licensed professional shareholder and pro forma professional practice financials of each licensed professional will be factors in determining if a California Professional Corporation is the most tax efficient structure to use when practicing in California.

Is a California Professional Corporation Right for You?

Based upon limited liability protection and tax efficiency, a California Professional Corporation is the best choice for most licensed professionals practicing in California.

To assist in the decision about whether a California Professional Corporation is the best business entity structure for your business, see “When to Use a California Professional Corporation” and “When Not to Use a California Professional Corporation” for more detailed information about choosing a business entity structure to practice in California.

If you are already practicing in a foreign LLC or foreign PLLC in California, see “12 Steps to Convert a PLLC to a California Professional Corporation“, and “Four Reasons Not to Convert Foreign LLC or PLLC to a California Professional Corporation” for more detailed guidance on moving from a foreign LLC or foreign PLLC to a California Professional Corporation.

If you are not already practicing in a foreign LLC or foreign PLLC, see “Four Things to Know About Starting Your California Professional Corporation“, “The 7 Steps for Forming a California Professional Corporation“, “How Long Does it Take to Form a California Professional Corporation?” for more detailed guidance on forming a California Professional Corporation for your professional practice.

To speak with a corporate attorney knowledgeable in matters of forming California Professional Corporations, schedule a consultation with the experienced corporate attorneys at San Diego Corporate Law.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}